SEC Staff Bulletin: Reasonably Available Alternatives, Costs & Documentation

Richard L Chen and Issa Hanna from Eversheds Sutherland met with InvestorCOM to discuss the SEC’s Guidance around assessing reasonably available alternatives, the consideration of costs, and whether firms need to document the evaluation of reasonably available alternatives.

==

Parham Nasseri [PN]: Richard, there is a specific call out in the Staff Bulletin: Standards of Conduct for Broker-Dealers and Investment Advisers Care Obligations that the assessment of reasonably available alternatives (RAA) or this cost comparison exercise needs to be more than just comparing share classes. If a firm asked you that question, how would you advise them?

Richard Chen [RC]: I think this was a Staff attempt to right-size the obligation with respect to the universe of investments that are considered RAAs and how advisors should think about right-sizing that obligation.

I think this component was designed to make sure advisors are aware that it is not simply that you look at the different flavors within the same investment. You must look broader than that. For instance, talking about this share class issue, if there is an ETF that accomplishes the same objectives for a client as the ETF or the mutual fund with the share class that you are considering then it is advisable that you look simply beyond a share class within the mutual fund that is appropriate. You have to think bigger. I think that this was the SEC’s attempt to show folks that you must broaden the alternatives that you are looking at.

[PN]: Thank you, Richard. Issa, our clients ask us this question very often: “Do costs need to be considered every single time?” The Staff Bulletin was fairly clear in their response. What do you make of that particular point?

Issa Hanna [IH]: In the text of Reg BI, the customer-specific best interest requirement explicitly requires you to consider cost among other things. Cost is not the be-all, end-all. There are absolutely circumstances where the lowest cost product is not in the retail customers’ best interest. You cannot just satisfy your Care Obligation by just recommending the lowest cost option. You have to think about what is in the retail customers’ best interest after considering their entire investment profile and what their particular needs are. So bottom line, I think the regulators have made it crystal clear that cost has to be a consideration. It is not the be-all, end-all, but it has to be considered as part of the process of arriving at a best interest recommendation.

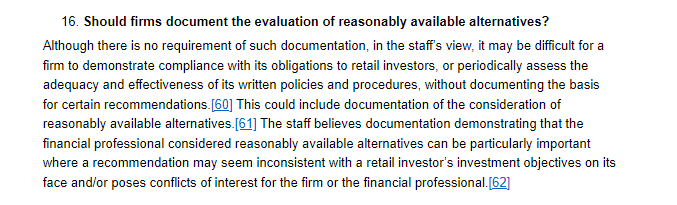

[PN]: There’s a question that comes up in every one of our webinars and in every conversation with our clients. It’s this notion that there needs to be documentation. (see FAQ 16) Should firms document the evaluation of reasonably available alternatives? Mr. Hanna, any thoughts?

Figure 1: SEC Staff Bulletin: Standards of Conduct for Broker-Dealers and Investment Advisors Care Obligations – FAQ 16

[IH]: In the Reg BI adopting release, there is not necessarily a requirement to document the basis for every single recommendation. This is explicitly stated. This is also reiterated in the Staff Bulletin, it’s what they lead off with and this FAQ 16 that it’s not necessarily a requirement. But then in the Reg BI adopting release, they state that broker dealers may wish to document an evaluation of a recommendation in certain contexts, especially in connection with complex, risky, or expensive products or in connection with significant investment decisions such as rollovers and account type recommendations.

I would say over time there has been a bit of a moving target here, based on some language in the adopting release where the Commission says broker dealers may wish to take a risk-based approach when deciding whether to document certain recommendations. That level of ambiguity regarding where that dividing line is between the risks that would necessitate documentation or not, is where you have some grey area.

That was followed up by the March 2022 Staff Bulletin where the Staff said it is their view that is difficult for a firm to assess periodically the adequacy and effectiveness of its policies and procedures, or to demonstrate compliance with its obligations to retail investors without documenting the basis for its account type and rollover recommendations.

There’s some difference in the language. They say it is a Staff view as opposed to a Commission requirement.

And then they introduced this new concept of the impact of a failure to document from a Compliance Obligation perspective. There is this component under Reg BI where the Staff says if you want to meet your Compliance Obligation, you must have something to test against. You must have some paperwork to look at, to see if you are in accordance with your policies and procedures. How do you show that your policies and procedures are being followed if you do not have contemporaneous documentation?

In the Staff Bulletin and FAQ 16, they reprised that concept about the Compliance Obligation. They say in the Staff’s view it might be difficult for a firm to demonstrate compliance with its obligations to retail investors or to periodically assess the adequacy and effectiveness of written policies and procedures without documenting the basis for certain recommendations.

They then say this could include documentation of the consideration of reasonably available alternatives. They finish the FAQ by stating the Staff believes documentation demonstrating that the financial professional considered RAA can be particularly important where a recommendation may seem inconsistent with the retail investors’ investment objectives on its face and/or poses conflicts for the firm or the financial professional.

That is a moving target so to speak, where the Staff is taking this view in a different direction. You might say this comes back to the principles-based nature of Reg BI or the statements by the Commission that you would take a risk-based approach when deciding whether or not the document. We’ve got a clear indication here; the Staff is looking for documentation in more and more expansive situations.

==

If you enjoyed this article, you can listen to the full webinar discussion. Watch the Replay 2023: SEC Guidance and Reasonably Available Alternatives.

If you would like to learn how InvestorCOM’s compliance platform is helping firms and financial professionals meet their Care Obligation requirement to assess reasonably available alternatives, sign up to see a demo